Tripadvisor (TRIP) Margin Improvement Challenges Bearish Profitability Narratives After Q3 2025 Results

Margin Improvement Challenges Bearish Profitability Narratives After Q3 2025 Results")

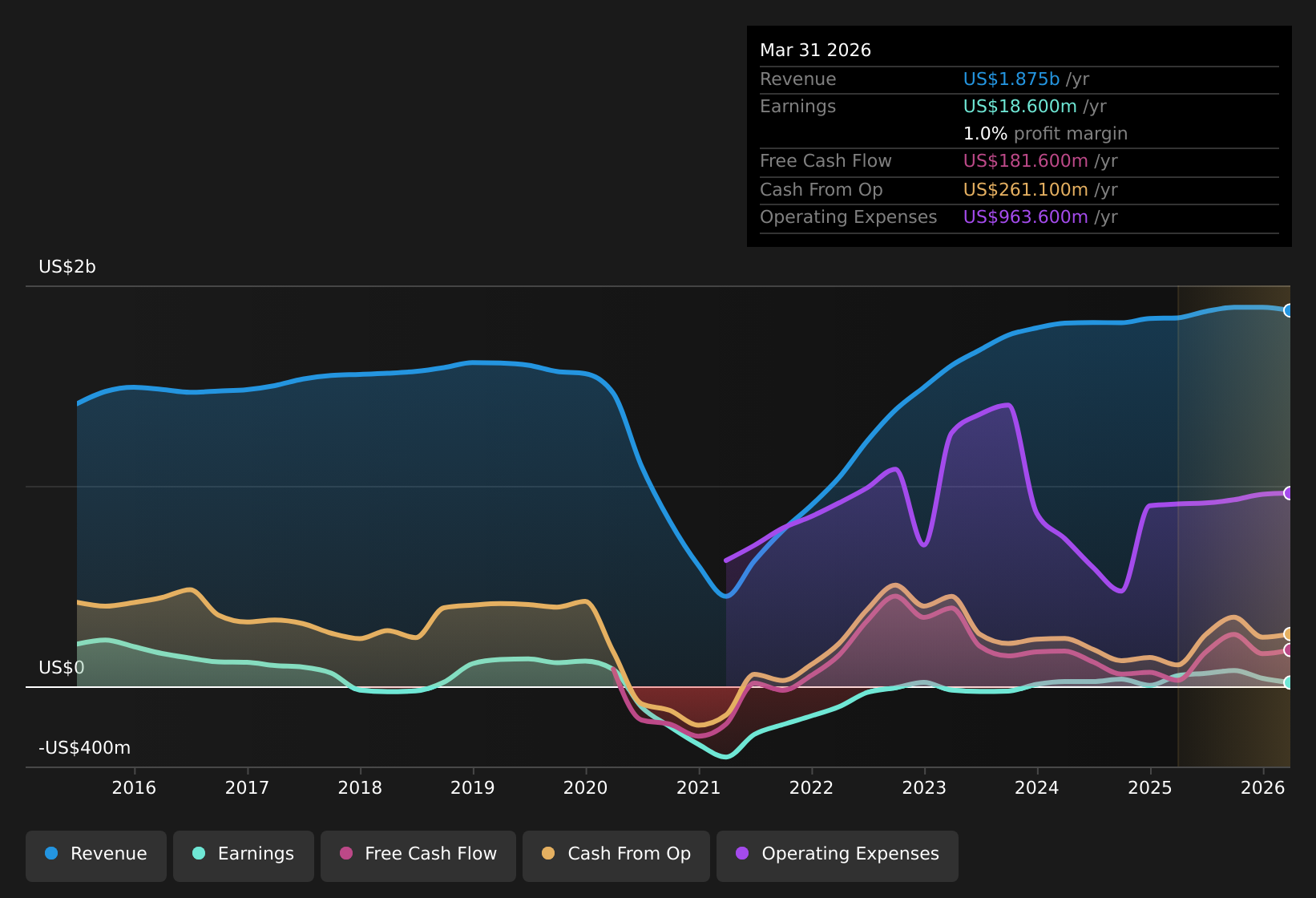

Tripadvisor (TRIP) has just posted its FY 2025 third quarter scorecard, reporting revenue of US$553 million and basic EPS of US$0.46, alongside net income of US$53 million. Trailing twelve month figures show revenue of US$1.9 billion, EPS of US$0.59 and net income of US$79 million, with a profit margin of 4.2% compared with last year’s 2%. The company’s quarterly revenue has moved from US$497 million in Q2 2024 to US$529 million in Q2 2025, and from US$532 million in Q3 2024 to US$553 million in Q3 2025. Over the same periods, EPS shifted from US$0.17 to US$0.29 and from US$0.28 to US$0.46, indicating earnings growth of 119.4% over the past year. Overall, margins are an important focal point here, as investors may weigh the stronger profitability against the more modest revenue growth profile.

See our full analysis for Tripadvisor.

With the latest results on the table, the next step is to consider how these margins and growth rates align with the dominant narratives around Tripadvisor and where the numbers might challenge those views.

See what the community is saying about Tripadvisor

Net margin at 4.2% while revenue grows 5.5% a year

- On a trailing twelve month basis, Tripadvisor generated US$1.9b of revenue with net income of US$79 million, which equates to a 4.2% net margin and compares with revenue growth of 5.5% a year versus the wider US market at 10.4% a year.

- Consensus narrative points to experiences platforms like Viator and TheFork as long term growth engines, and the current 4.2% margin creates a mixed picture, with:

- Revenue growth running at 5.5% a year and below the 10.4% US market forecast, which challenges the idea of Tripadvisor consistently outgrowing the market.

- At the same time, trailing net margin has moved from 2% to 4.2%, which supports the view that newer revenue streams and product focus can support healthier profitability even with more modest top line growth.

EPS swings and one off US$33m loss in the background

- Quarterly EPS has moved from a loss of US$0.08 in Q1 2025 to US$0.29 in Q2 2025 and US$0.46 in Q3 2025, while the last 12 months include a material one off loss of US$33 million that affects reported net income.

- Bears argue that Tripadvisor’s earnings power is fragile and vulnerable to rising costs and competition, and the recent figures give you data points on both sides of that argument:

- The swing from a US$11 million loss in Q1 2025 to US$53 million of net income in Q3 2025 supports the bearish concern that results can be volatile, especially when one off items like the US$33 million loss are part of the trailing period.

- At the same time, trailing EPS of US$0.59 and 119.4% earnings growth over the past year push back a bit on the idea of structurally weak profitability, because the business is currently profitable even with that one off charge in the numbers.

Look at how skeptics frame these EPS swings and one off items, then decide whether you agree with their caution through the full bear thesis for Tripadvisor: 🐻 Tripadvisor Bear Case

P/E of 15.3x and DCF fair value far above US$10.32

- Tripadvisor trades on a P/E of 15.3x, slightly below the peer average of 16.4x but above the Interactive Media & Services industry at 10.8x, while a DCF fair value of US$32.91 sits well above the current share price of US$10.32.

- Bullish investors see recent 119.4% earnings growth and that large gap to the US$32.91 DCF fair value as supportive of their view, and the latest numbers give them some specific talking points:

- Trailing revenue of US$1.9b and net income of US$79 million, plus forecasts for roughly 19.3% annual earnings growth, line up with the bullish idea that earnings can grow faster than the top line as margins improve from today’s 4.2% level.

- The fact that the P/E of 15.3x sits below peers at 16.4x, yet the DCF fair value is more than triple the current US$10.32 share price, is exactly the kind of valuation gap bulls point to when they argue that the market is not fully reflecting earnings and cash flow potential.

If you want to see how optimistic investors connect this valuation gap to future earnings power, check out the full bullish narrative built around Tripadvisor’s latest numbers: 🐂 Tripadvisor Bull Case

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Tripadvisor on Simply Wall St. Add the company to your watchlist or portfolio so you’ll be alerted when the story evolves.

See the numbers differently? If this data is pointing you in another direction, shape that view into your own narrative in just a few minutes: Do it your way

A great starting point for your Tripadvisor research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Explore Alternatives

Tripadvisor’s 5.5% annual revenue growth, which runs below the wider US market, and its modest 4.2% net margin highlight that growth and profitability are not especially strong.

If that mix of slower revenue momentum and only moderate earnings power leaves you uneasy, use our 55 high quality undervalued stocks to quickly find companies where stronger fundamentals may already be paired with more appealing pricing today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Tripadvisor might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

link